At RaptorCon 2026, Jason Kaminsky, CEO of kWh Analytics, gave a candid look at how the insurance industry actually evaluates solar risk, and why many asset owners are leaving money on the table by not engaging with it more directly. Solar insurance is a corner of a $7 trillion global industry that, by Jason's own admission, is "very opaque" and "by design" hard to understand. But as one of the largest line items on an operating P&L, minimizing this cost can have a material effect on an operating budget. That is why it is essential for asset owners to engage directly with their insurers in order to build robust, technically sound risk management programs.

Here are three takeaways that stood out from the talk that can help asset owners who are thinking about how they can influence their insurance T&Cs:

1. Hail Stow Is the Single Most Underwriteable Operational Practice

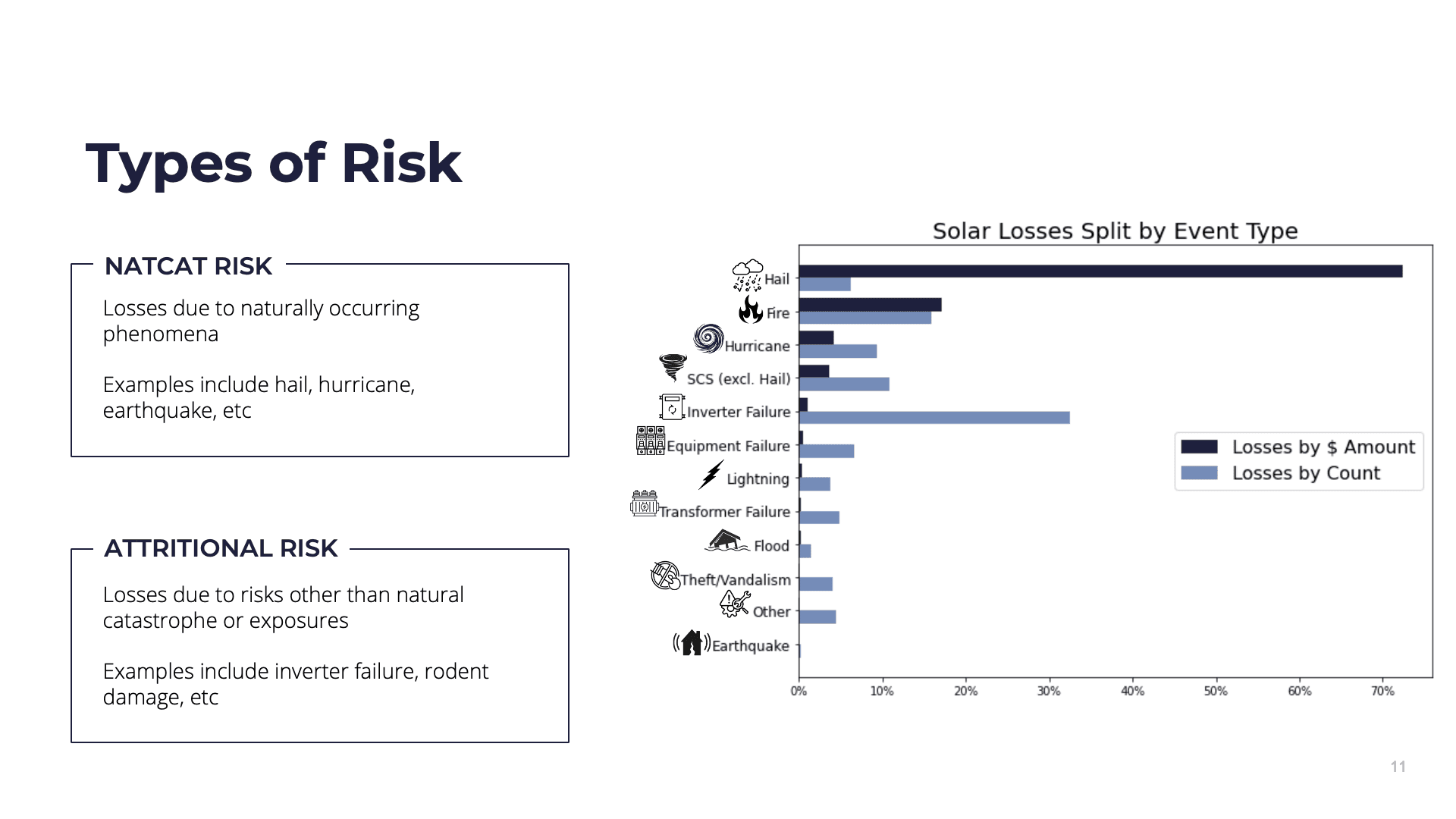

Jason walked through a real underwriting example that drove this point home. For a large project with a strong hail protocol — reasonable tilt, good module glass, and roughly 90% compliance with past hail stow events — kWh Analytics priced in a 72% reduction in expected hail damage relative to a non-compliant baseline. In Jason's words, "72% to me is a pretty material reduction for what is often a pretty expensive component of these policies."

That number matters because hail is the dominant pricing driver in many solar markets. The 2019 Midway project in Texas, an $80 million hail loss that the industry had not modeled for, was the inflection point that hardened the entire renewables insurance market. Since then, kWh Analytics has built underwriting models that price differently based on glass thickness and stow compliance — but only when that data is communicated to the underwriter. Sites that don't surface this data are assumed to be average or below by default.

The actionable takeaway: if your sites have a hail stow protocol, the operational compliance rate is a number worth tracking and surfacing at every renewal.

Check out kWh Analytics’ 2026 Solar Risk Assessment Report here, which includes a chapter from Raptor Maps on substation shutdown risk.

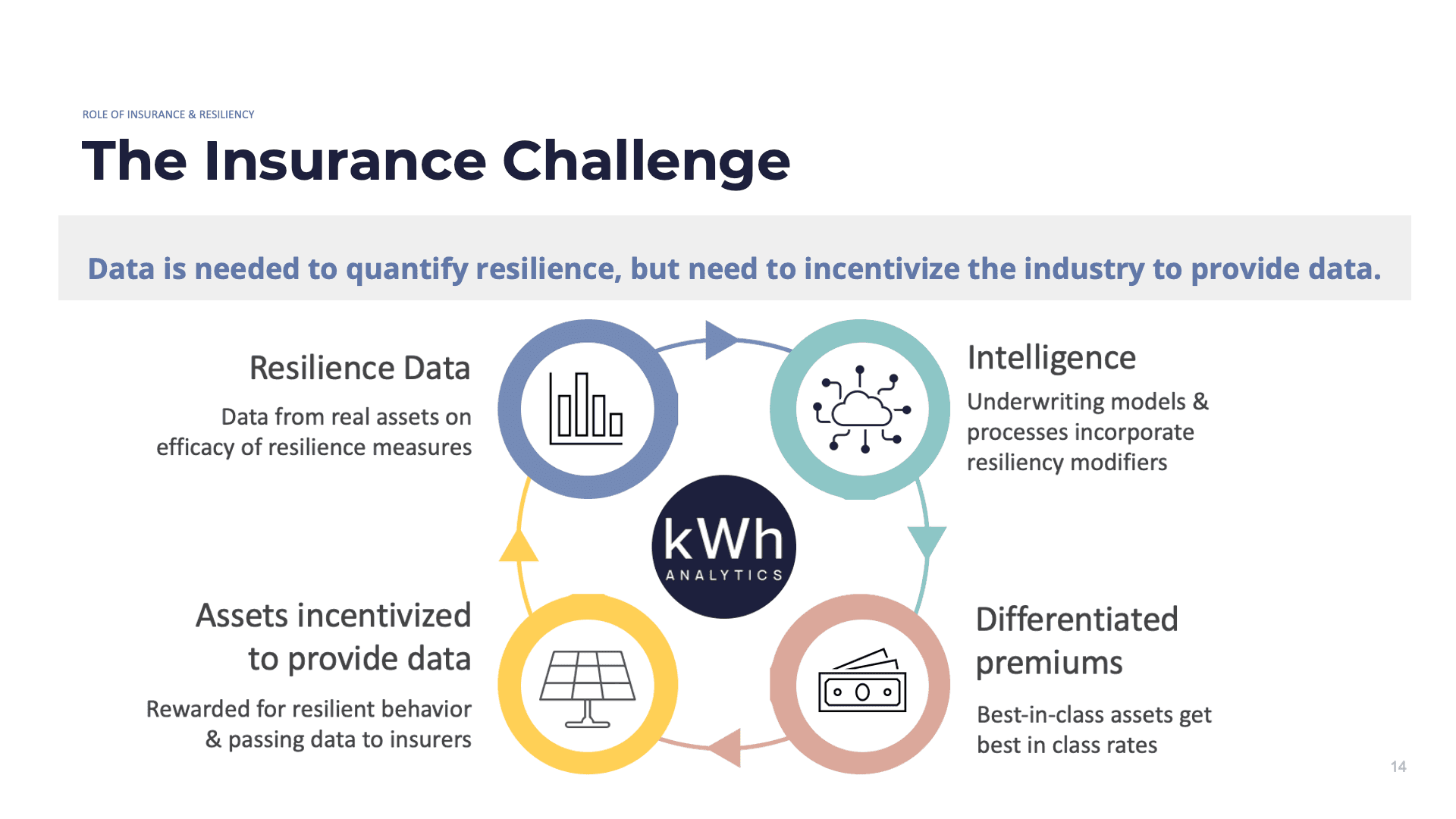

2. The Burden of Proof Sits With the Asset Owner

This was the throughline of Jason's talk, and it has direct operational implications. Insurance underwriters cannot price what they cannot see. When a submission lacks documentation — equipment specs, hail stow compliance rates, vegetation management practices, post-event response capabilities — the underwriter's only safe assumption is that the asset is average or below average, and the rate reflects that. Jason was blunt about how often this happens: kWh Analytics regularly receives submissions on multi-billion-dollar portfolios where basic equipment data is missing for a third of the assets in scope.

What this looks like in practice is a shift in mindset. Documentation isn't paperwork for the broker. It's evidence that supports a pricing argument. Equipment specs, drone-based inspection records, hail stow logs, vegetation management cadence, transformer monitoring data — all of this is underwriteable, but only if it's captured systematically and surfaced in a digestible format. The companies who treat documentation as a continuous program, rather than a once-a-year scramble, are the ones who get credit for the work they're already doing.

3. Underwriter Knowledge Is Improving — and the Curve Is Steepening

Jason was direct about how much the insurance industry has had to learn in a short period of time. Before 2019, solar insurance was cheap, plentiful, and largely undifferentiated. The Midway loss changed that, and the four years since have been spent working through how to model risk on an asset class that no one had a real loss history for. kWh Analytics' read on the current state: the market is in "inning one or two" of smart coverage, where data and best practices are starting to translate into meaningful pricing differentiation.

The trajectory matters. Four years ago, the average solar underwriter was not asking about module glass thickness. Today, leading underwriters are pricing differentially for it. Three to four years from now, Jason expects general pricing differentiation across the market for hail-prone regions like Texas, with operational practices like stow compliance, vegetation management, and post-event response all becoming standard inputs to underwriting models.

For asset owners, this trajectory reframes the ROI question on resilience investments. The relevant question is whether you'll be in the cohort of operators who can demonstrate best practices when underwriting catches up. Investments in operational data infrastructure made today position the portfolio for the pricing environment of three to four years from now.

The Bottom Line

The throughline across all three takeaways is the same: insurance pricing responds to documented best practices, and the burden of proof sits with the asset owner. In a market where operational data is increasingly capturable through autonomous inspection, IoT-enabled trackers, and structured platforms, the operators who systematize that documentation will pull ahead of those who don't — both in claim outcomes and in renewal economics.

For more detail on the trends shaping solar insurance underwriting, catch the full replay of the session here and check out kWh Analytics’ 2026 Solar Risk Assessment Report here.

Next steps

From the civil engineering on your site down to the wiring on the back of your panels, the Raptor Solar platform provides you detailed, up-to-date data on the conditions and performance of your solar fleet so that your team has the intel they need to do their jobs effectively, quickly, and safely.